Blockchain in Insurance: 5 Powerful Ways It’s Disrupting the Industry

The insurance industry, traditionally bogged down by paperwork, fraud, and slow claims processing, is ripe for transformation. Enter blockchain technology, a disruptive force that could radically reshape how insurers operate. In this article from bit2050.com, we explore five major ways blockchain in insurance is revolutionizing the sector.

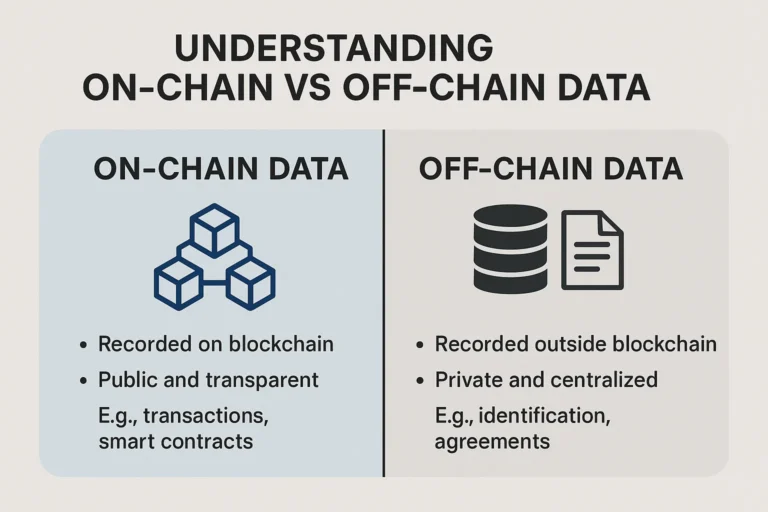

🔐 1. Fraud Detection and Prevention

Insurance fraud costs the global economy billions each year. Blockchain provides an immutable and transparent ledger, making it easier to track claims and prevent duplicate or fake filings. By recording every transaction on-chain, insurers can verify claim history and significantly reduce fraudulent activities.

📄 2. Smart Contracts for Instant Claims

Smart contracts allow policies to be automatically executed when specific conditions are met. For example, in travel insurance, a smart contract could trigger an automatic payout if a flight is delayed. This eliminates manual approval and speeds up claim settlements.

🔍 3. Enhanced Transparency for Policyholders

Customers often complain about the lack of transparency in insurance terms. Blockchain ensures every change and condition in a policy is recorded and visible. This builds trust, improves customer satisfaction, and reduces legal disputes.

🔗 4. Efficient Reinsurance Processes

Reinsurers and insurers often suffer from data mismatches. Blockchain allows real-time data sharing, reducing delays and errors in the reinsurance chain. It also simplifies auditing and compliance by creating a clear history of policy data and claims.

💰 5. Lower Operational Costs

With automated processes, fewer intermediaries, and faster settlements, blockchain helps cut down administrative costs. Over time, this could lead to more affordable premiums and increased competitiveness in the market.

Real-World Use Cases

-

Etherisc is creating decentralized insurance products on blockchain.

-

AIG and IBM have explored smart contract-based policies.

-

Lemonade uses blockchain to process claims faster and with more transparency.

Final Thoughts

The integration of blockchain in insurance isn’t a matter of if, but when. As insurers begin to adopt this groundbreaking technology, early adopters will gain a serious competitive edge. For more insights into blockchain’s impact on finance and beyond, keep reading at bit2050.com.

✅ FAQs – Blockchain in Insurance

❓ What is blockchain in insurance?

It refers to using blockchain technology to manage insurance policies, claims, and transactions in a secure, transparent, and automated way.

❓ How does blockchain prevent insurance fraud?

Blockchain’s immutable ledger ensures all claims and policyholder data are recorded transparently, making it difficult to file duplicate or fake claims.

❓ Are smart contracts legal in insurance?

Yes, in many jurisdictions, smart contracts are recognized legally. However, their usage depends on regional regulations and compliance standards.

❓ Will blockchain eliminate insurance agents?

Not entirely. While blockchain automates many processes, agents can still provide personalized service and guidance in complex cases.

✅ Tags:

blockchain, insurance, fintech, smart contracts, blockchain use cases, decentralized insurance, insurance technology, blockchain in insurance