🧠 Introduction

Debt snowball vs avalanche method: When it comes to paying off debt, there are two strategies that dominate the personal finance world: the Debt Snowball and the Debt Avalanche. Both work — but they work differently.

So which method is right for you? This guide breaks down the Debt Snowball vs Avalanche method, comparing pros, cons, and ideal use cases, so you can make the smartest financial move today.

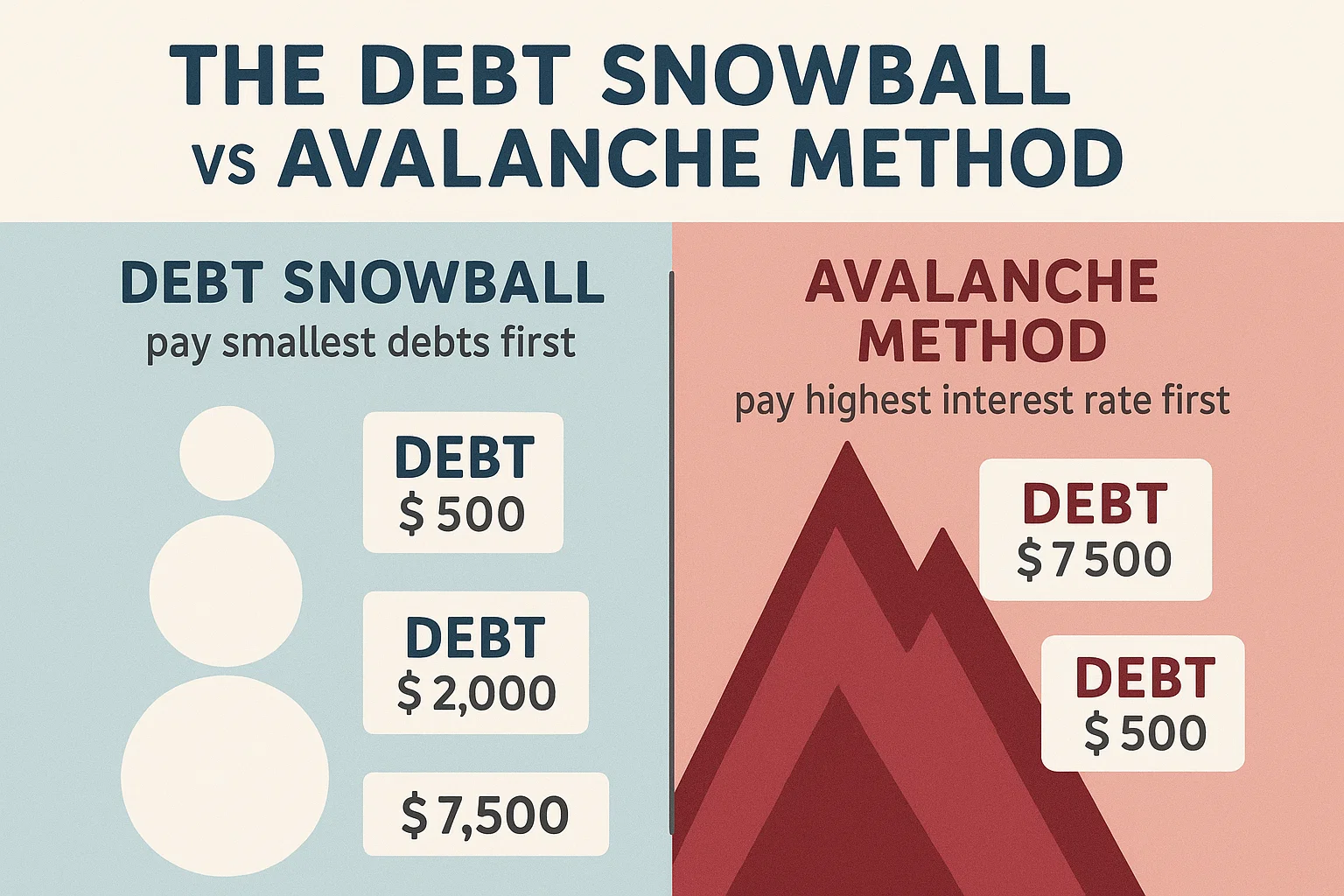

❄️ What Is the Debt Snowball Method?

The Debt Snowball Method focuses on paying off your smallest debts first, regardless of interest rate. Once a small debt is cleared, you “roll” that payment into the next smallest debt — like a snowball gaining size and speed.

🔹 Example:

-

₹5,000 credit card ➡️ First

-

₹10,000 personal loan ➡️ Next

-

₹30,000 car EMI ➡️ Last

You gain emotional wins early, building motivation to keep going.

🔥 What Is the Debt Avalanche Method?

The Debt Avalanche Method tackles your highest interest rate debt first, saving you the most money in the long run.

🔹 Example:

-

36% credit card ➡️ First

-

18% personal loan ➡️ Next

-

10% car loan ➡️ Last

This approach is mathematically optimal, reducing total interest paid.

⚖️ Debt Snowball vs Avalanche Method – Side-by-Side Comparison

| Criteria | Snowball Method | Avalanche Method |

|---|---|---|

| Focus | Smallest balance first | Highest interest first |

| Speed of motivation | Fast (quick wins) | Slower, but logical |

| Total interest saved | Less savings | More savings |

| Ideal for | Emotional motivation | Mathematically minded |

| Ease of use | Very easy to follow | Slightly more complex |

🔗 Useful Links – bit2050.com

🌐 Resources

❓ FAQ – Debt Snowball vs Avalanche Method

Q1. Which method helps pay off debt faster?

The Avalanche method is usually faster in total time and money saved, but only if you stay motivated.

Q2. Which is better for beginners?

The Snowball method is beginner-friendly and ideal if you need emotional wins to stay on track.

Q3. Can I combine both strategies?

Yes! Some people use a hybrid method — start with Snowball for quick wins, then switch to Avalanche to save more interest.

Q4. What if I have only one large debt?

Use the Avalanche method if interest is high. If it’s low-interest and long-term, consider investing alongside slow repayment.

Q5. Are there apps to automate these methods?

Yes. Try Goodbudget, YNAB, or India-based apps like ET Money and Walnut.

🏁 Final Thoughts

Choosing between the debt snowball vs avalanche method depends on your personality, income, and what motivates you more — fast results or long-term savings.

💡 No matter which path you choose, consistency is key. Ready to destroy debt and build wealth?

👉 Visit bit2050.com for more tools, guides, and real-money advice.