🧾 What is a Loan Against Property (LAP)?

A Loan Against Property (LAP) is a secured loan where you pledge your residential, commercial, or even rented property as collateral. It’s a popular way to raise high-value funds at lower interest rates compared to unsecured loans.

But like any financial decision, it comes with both strong advantages and serious drawbacks. Here’s a complete breakdown to help you make an informed choice.

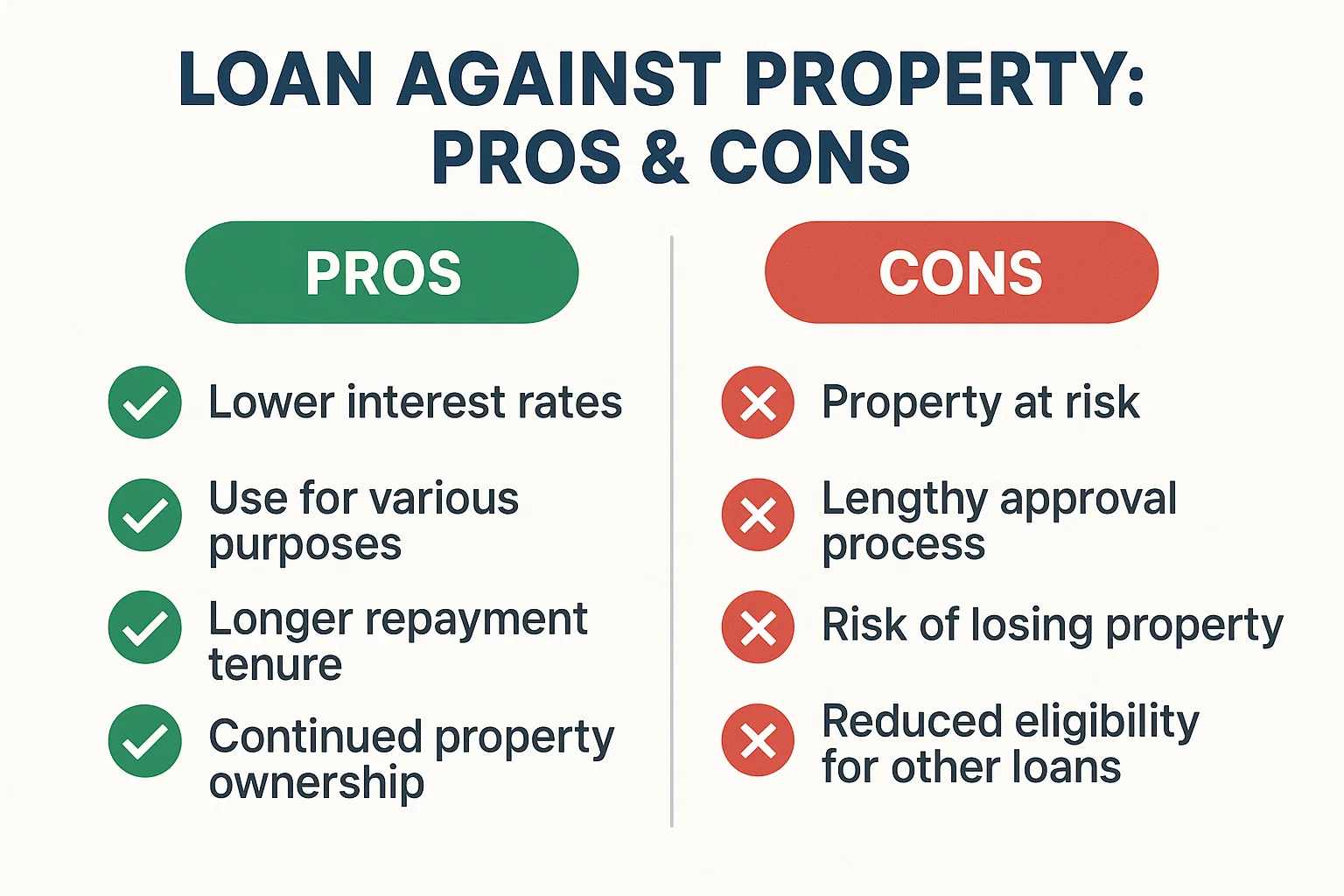

✅ 7 Powerful Pros of Loan Against Property

1. Lower Interest Rates

LAP interest rates typically range between 9%–12%, which is much lower than personal loans (which go up to 16–24%).

2. Higher Loan Amount

You can get up to 60–75% of your property’s current market value — ideal for business expansion, weddings, or education abroad.

3. Longer Tenure

Loan terms can go up to 15–20 years, making EMIs more affordable and easier to manage over time.

4. Multiple Usage

No restrictions on end-use — whether it’s business, medical expenses, or debt consolidation.

5. Property Remains Yours

You retain ownership and use of the property during the loan term, unless you default.

6. Improves Credit Mix

A LAP adds diversity to your credit profile, boosting your credit score if paid on time.

7. Tax Benefits

You may get tax deductions if the loan is used for business purposes or for house renovation (under Section 24(b)).

❌ 5 Hidden Cons of Loan Against Property

1. Risk of Losing Your Property

If you fail to repay, the lender has the right to auction the property.

2. Lengthy Approval Process

Since it’s a secured loan, documentation and property valuation can take 1–3 weeks.

3. Not Ideal for Short-Term Needs

Due to the long processing time, it’s not suitable for urgent or small funding requirements.

4. Legal Issues with Property

Any disputes or unclear titles can delay or reject your application.

5. Interest Still Accrues During Moratorium

If you opt for deferred EMIs, interest continues to accumulate, increasing the final cost.

🧠 When Should You Consider a Loan Against Property?

-

✅ Need ₹10+ lakhs at low interest

-

✅ Have a clear-titled property

-

✅ Can repay over 10–15 years

-

✅ Want funds for business, not personal luxuries

🔗 Useful Links – bit2050.com

🌐 Resources

❓ FAQ – Loan Against Property

Q1. Can I apply for a loan against a rented property?

Yes, if you’re the legal owner, rented commercial/residential properties can be pledged.

Q2. Is CIBIL score important for LAP?

Yes, most banks require a CIBIL score of 700+ for faster approval and better interest rates.

Q3. Can I prepay a LAP early?

Yes. But some banks may charge a prepayment penalty. Check the loan terms before applying.

Q4. What documents are needed?

-

Property papers (ownership proof)

-

Income documents (ITR, salary slips)

-

ID/address proof

-

No-objection certificate (in case of co-owners)

Q5. Is LAP better than a personal loan?

If you need large funds and have property, LAP is usually cheaper and longer-term than a personal loan.

✅ Final Thoughts

A loan against property is a powerful financial tool — if used wisely. It’s ideal for planned, large-scale expenses but risky if you cannot maintain timely repayments. Always compare offers, read the fine print, and calculate your repayment ability.

Want help comparing loan offers? Bookmark 👉 bit2050.com for expert guides, tools, and crypto-finance insights.