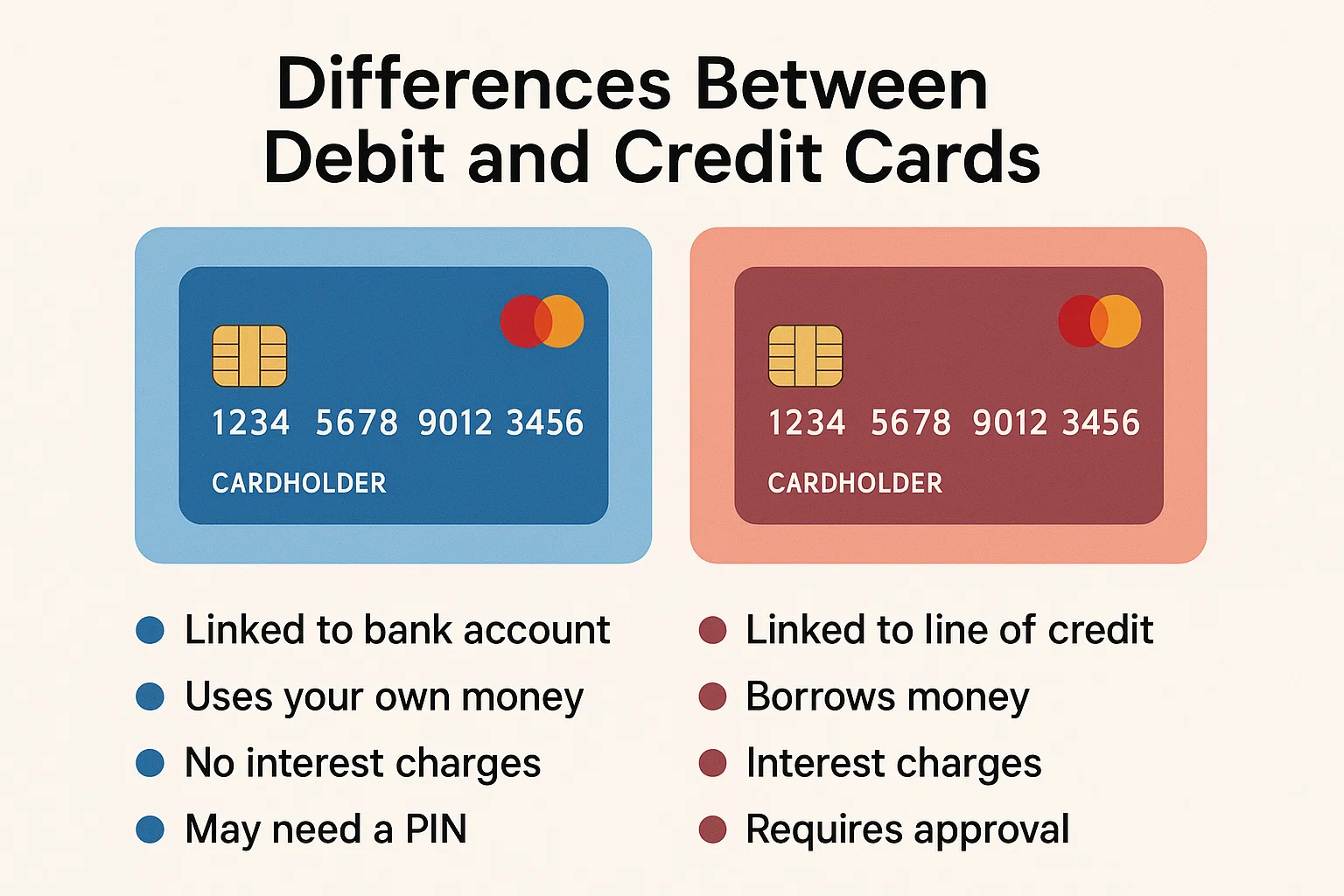

💳 Top 7 Differences Between Debit and Credit Cards You Must Know

In the age of cashless transactions, understanding the differences between debit and credit cards is essential. Both plastic cards may look identical but serve entirely different financial functions.

Whether you’re a student, working professional, or entrepreneur, this guide from bit2050.com will help you make informed decisions.

🆚 1. Source of Funds

🧾 2. Monthly Bills & Repayment

💰 3. Interest Charges

⚠️ 4. Risk of Debt

🛍️ 5. Rewards & Offers

-

Debit: Basic or limited reward programs.

-

Credit: Higher rewards, cashback, travel points, lounge access, etc.

🔐 6. Security & Fraud Protection

📈 7. Impact on Credit Score

✅ Useful Links – bit2050.com

🌐 Resources

❓ FAQ – Differences Between Debit and Credit Cards

Q1: Which is safer for online transactions?

Credit cards are usually safer due to better fraud protection and dispute mechanisms.

Q2: Can I use a credit card like a debit card?

You can pay using a credit card, but you’ll need to repay the amount later with or without interest.

Q3: Which one is better for building credit history?

Only credit cards affect and help build your credit score.

Q4: Are debit cards interest-free?

Yes. Since they deduct money directly from your bank, there’s no interest involved.

Q5: Can I withdraw cash from both?

Yes, but credit card withdrawals involve extra fees and interest, while debit card withdrawals are generally free up to a limit.

🏁 Final Thoughts

Understanding the differences between debit and credit cards empowers you to manage your money better. Choose the card based on your financial habits, goals, and responsibility level. For more such comparisons and smart money tips, visit bit2050.com.